Unlocking Value in Titan Cement: U.S. Listing Brings European Assets for Free

50% Upside in less than a year

Investment Report

Key points:

Undervalued U.S. Assets: Titan's planned U.S. asset listing alone is estimated at around €3.36 billion, which exceeds the company’s current total enterprise value of $3.1 billion, meaning the European business comes essentially "free" at current valuations.

European Growth Potential: The European division, valued conservatively at €1.3 billion, offers double-digit revenue growth potential with margin expansion opportunities, operating in faster-growing economies than the U.S.

Strong U.S. Market Outlook: The U.S. cement and concrete market is expected to remain robust, supported by political commitment to housing construction, which would drive demand and potentially increase the U.S. asset valuation.

Long-Term Catalysts: Future European demand could rise due to factors like economic recovery in Greece and reconstruction in Ukraine, adding upside potential.

1. Introduction:

Titan Cement is a key player in the global cement market, operating across a range of regions, including the United States, Southeastern Europe (SEE), Western Europe (WE), Greece, and the Eastern Mediterranean (EMED). This geographic reach positions Titan to serve diverse and growing markets. In a bold strategic move, the company plans to list its U.S. assets separately, aiming to unlock value for shareholders. With a projected valuation of around 3.3 billion euros for these U.S. assets alone, this listing implies that investors could essentially acquire Titan's extensive European operations for free.

The timing is also intriguing. A mix of central banks lowering interest rates and an expected increased pace in new construction due to the housing crisis suggests potential for increased demand for cement and concrete as economic conditions and political decisions fuel new constructions. Additionally, there’s the long-term potential of European cement demand rising significantly once reconstruction in Ukraine begins, which would be a boost to companies like Titan. Beyond cement, Titan has also expressed intentions to diversify further, reducing its exposure to the cement market by expanding other business segments. This strategic shift could position Titan to weather industry cycles and as a result maintain more stable margins.

2. Financials:

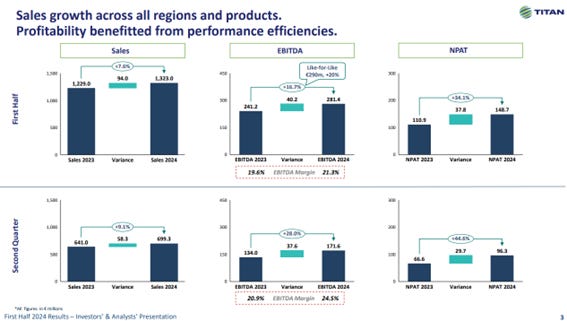

Titan Cement has demonstrated strong financial growth, consistently expanding its EBITDA margins year-over-year. The company has managed to grow its revenues steadily while also returning value to shareholders through share buybacks and dividend payments. Over the past decade, Titan has more than doubled its revenues and, impressively, achieved a tenfold increase in earnings per share (EPS). This remarkable EPS growth has been driven by margin improvements and strategic share buybacks, showcasing Titan's disciplined approach to capital allocation.

Even though margins are volatile the long-term trend is clearly positive.

EBITDA margin expansion has enabled Titan to achieve high double-digit profit growth, supported by steady sales growth in the mid to high single digits. Recent performance has been particularly strong, with the first and second quarters showing significant EBITDA gains, reflecting the company’s continued focus on efficiency and profitability. Titan’s robust financials underscore its resilience and growth potential, positioning it well for future opportunities in both established and emerging markets.