Theon International: Aggressive Growth in the Defense Sector.

Investment Report

AMS: THEON

Market capitalization: 801 million euros

Stock price: 11.38€

P/E ratio: 19

Sector: Defense

Key points:

The company operates in a market expected to grow at an 11.5% annual rate.

Christian Hadjiminas, the CEO, owns 10% of the company and brings decades of experience in the sector.

THEON International has achieved a 50% compound annual growth rate (CAGR) in revenue over the last five years.

The company consistently delivers high returns on capital, a testament to its strong focus on efficient capital allocation.

THEON International is currently undervalued compared to its industry peers.

Index:

Introduction

Business model

Competitive advantages

Dividend payout

Sector analysis

Leadership

Backlog of orders

Financial Performance

Thesis

Valuation

Risks

Conclusion

1. Introduction:

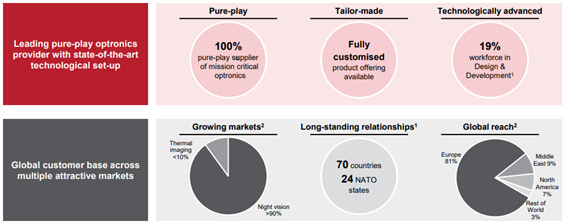

THEON International PLC is a leading manufacturer of night vision and thermal imaging systems, primarily catering to defense and security applications worldwide. Founded in Greece in 1997, the company has rapidly expanded its geographical presence with offices in Greece, Cyprus, the USA, UAE, Switzerland, and Singapore, as well as production facilities in Athens, Wetzlar (Germany), and Plymouth (USA). THEON's global operations are supported by a robust network that serves 69 countries, including 26 NATO members, and has more than 150,000 systems in service with armed and special forces globally.

In February 2024, THEON successfully listed its shares on the regulated market of Euronext Amsterdam, marking one of the first IPOs in Europe that year and raising nearly €100 million in gross proceeds. The funds raised are intended to accelerate THEON's growth through new investments and acquisitions, reinforcing its status as a global leader in the industry.

THEON has demonstrated remarkable growth, achieving a 53% year-on-year revenue increase in FY2023 to €218.7 million, with an adjusted EBIT margin of 26%. The company's rapid growth is supported by a strong order intake of €506 million, representing a 51.7% increase from the previous year, and a soft order backlog of €540.2 million—equivalent to 2.5 times the revenue of 2023. This growth is driven by a rising global demand for advanced night vision systems, particularly in light of increasing defense budgets and procurement programs worldwide.

The addressable market for night vision and thermal imaging systems is expected to grow significantly, fueled by heightened geopolitical tensions and an international trend recognizing the importance of night fighting capabilities. THEON is well-positioned to capitalize on this market growth with its cutting-edge product portfolio, which includes innovative solutions like the TALOS multisensory system and advancements in image fusion and augmented reality technologies.

Despite its expected future growth trajectory and strong market positioning in a market that is expected to grow at a 11.5% CAGR over the following years, THEON remains attractively valued, trading at a ≈12 forward P/E ratio. The company is led by CEO Christian Hadjiminas, who brings extensive experience and expertise in the industry, ensuring strategic leadership and a commitment to innovation and customer satisfaction.

Overall, THEON International PLC's strategic initiatives, robust financial performance, and leadership in a rapidly growing market make it a compelling investment opportunity with significant potential for future growth and value creation.

2. Business model:

THEON International PLC is a leading manufacturer specializing in night vision and thermal imaging systems, providing critical solutions primarily for defense and security applications on a global scale. As a pure play optronics provider, THEON focuses on delivering fully customized products tailored to meet the specific needs of its clients. This approach ensures that the company remains agile and responsive to evolving market demands and technological advancements.

2.1 Market leadership:

Europe:

THEON has an estimated >50% market share of the European night vision goggles market, being the market leader in Germany and Belgium and growing their revenues on Latvia, Austria, Sweden and Italy.

US:

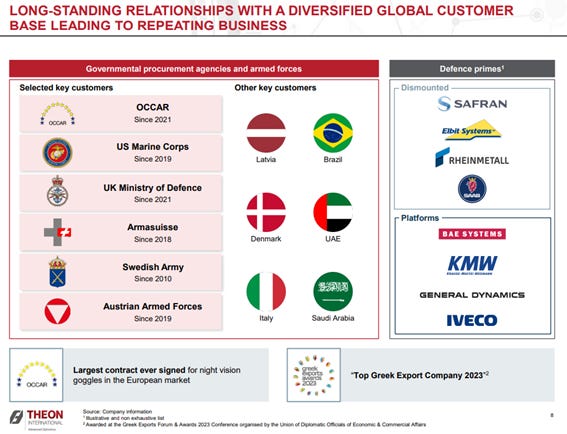

THEON International PLC has significantly bolstered its presence in the U.S. market through strategic initiatives and partnerships. The company was recently awarded a second contract with the United States Marine Corps (USMC), set to run through 2028. This contract builds on the success of THEON's first USMC contract, under which approximately 17,000 units were delivered since 2019. Additionally, THEON has formed a strategic partnership with EOTECH, a well-known optics company, to expand sales into the U.S. law enforcement and commercial markets.

MENA:

The company is the market leader in UAE for night vision googles with more than 50% of the total market share. They are growing their positioning in Saudi Arabia and Kuwait. Furthermore, they are a key supplier to Morocco for customized devices

2.2 Geographical distribution

The company's primary clientele consists of government entities, reflecting its strategic positioning within the defense sector. Geographically, THEON's revenue distribution is heavily skewed towards Europe, which accounts for 81% of its business. The Middle East contributes 9%, North America 7%, and the remaining 3% comes from other regions worldwide. This distribution highlights THEON's strong presence and influence in the European market, furthermore the company will increase their revenues coming from the US thanks to the five-year 500$ million IDIQ (indefinite delivery/indefinite quantity) contract for the supply of the Squad Binocular Night Vision Goggle systems to the US Marine Corps that Elbit Systems of America is awarded, with THEON as their subcontractor.

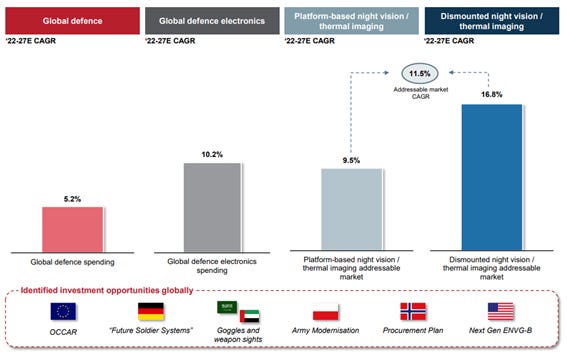

In recent years, global geopolitical events have spurred a substantial rise in defense spending across virtually all nations, with each region driven by its specific threat landscape. This has translated into significant growth in defense budgets worldwide, projected to increase by 5.2% annually over the next years. Within this context, the defense electronics segment, in which THEON operates, is expected to grow even more rapidly at approximately 10% per annum. More specifically, THEON's addressable market, encompassing dismounted and vehicle-based electro-optical and infrared (EO/IR) systems, is anticipated to experience accelerated growth at an 11.5% compound annual growth rate (CAGR), driven by a renewed focus on dismounted capabilities projected to grow over 16% annually.

THEON’s business model capitalizes on these trends, as it offers high-margin products and services designed to meet the sophisticated needs of its clients. The company places a strong emphasis on sound management practices, risk prevention, cost reduction without compromising quality, and maintaining consistency and reliability for its customers and partners. These values have long been integral to THEON's operations and have enabled it to establish itself as a trusted partner in the field.

3. Competitive advantages:

THEON International has a unique position in the defense sector, leveraging its strengths to maintain and grow its market share. The company's competitive advantages are key for THEON to be able to maintain their high margins over time.

Strong reputation and reliability

THEON International has established a sterling reputation for reliability and excellence in delivering cutting-edge night vision and thermal imaging systems. The company consistently fulfills its promises, which has resulted in a high level of trust among its clients. This trust is essential in the defense sector, where reliability and performance are critical. By consistently meeting client expectations, THEON reinforces its status as a reliable partner in the industry.

High-demand product portfolio

The demand for advanced night vision and thermal imaging systems is rising globally due to geopolitical tensions and increased defense budgets. THEON's product offerings are at the forefront of this demand. The company's focus on innovation and technological advancement ensures that its products remain highly sought after, positioning THEON as a leader in the market.

Global blue chip customer base

THEON International boasts a diverse and prestigious customer base, including many government agencies. This extensive network of long-standing relationships spans across 69 countries and includes 26 NATO members, underscoring the company's global reach and influence. These relationships are built on years of successful collaboration and delivery, ensuring a steady demand for THEON's products and services. THEON is already the market leader of multiple of this countries and a key supplier for night vision and thermal imaging systems for a lot of them.

Experienced leadership and skilled workforce

The leadership team at THEON, led by CEO Christian Hadjiminas, has an impressive track record in the defense industry. This experience is complemented by a highly skilled workforce that is adept at addressing the complex needs of the defense sector. THEON's commitment to talent development is evident in its investment in training and upskilling programs, which help maintain a competitive edge by ensuring that employees are equipped with the latest industry knowledge and skills. This combination of strong leadership and a skilled workforce drives innovation and operational excellence, further solidifying THEON's position as a market leader.

Overall, THEON International's strong reputation, high-demand products, extensive customer base, and experienced leadership contribute to its competitive advantages. However, competitors may try to enter the industry due to the high margins the sector offers.

4. Dividend payout:

The company will pay 40% of net earnings as a dividend for this year 2024 and expects the dividend payout to be between 30-40% in the medium term.

Although I prefer that management makes use of buybacks as a way to return value to shareholders, a conservative dividend might attract dividend investors and improve the valuation of the company. Moreover, the payout is not too high and allows the company to reinvest their profits.

5. Sector analysis:

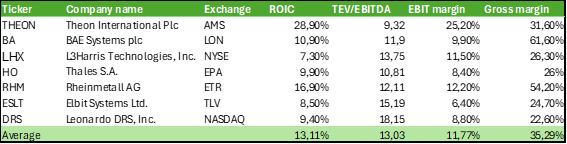

When comparing the company to its competitors, it is evident that THEON International has much greater returns and margins than them. The company reports exceptionally high EBIT margins compared to industry averages, a sign of efficient management and effective cost control strategies.

Management's confidence in maintaining EBIT margins in the mid-twenties further underscores the company's robust operational framework and strategic positioning within the market. It is possible that new competitors might enter the market due to the compelling returns that are being offered.

One notable financial metric where THEON leads is Return on Invested Capital (ROIC), which is significantly higher than that of its peers. This indicates that THEON is not only generating superior profits from its investments but is also managing its capital more effectively than competitors.

Regarding valuation, THEON's market pricing appears relatively inexpensive, especially when considering its superior margins and ROIC relative to its peers. Such an attractive valuation coupled with strong financial performance suggests that THEON International could be undervalued and present a great investment opportunity for value investors.

6. Leadership:

Christian Hadjiminas, President of EFA GROUP, has a distinguished educational background with a B.A. in Economics from Columbia University and an MBA in Business and Finance from Wharton Business School, University of Pennsylvania. His career began at Phibro-Salomon Inc., where he served as a Senior Trader until 1987. He then founded his first company in New York and relocated his business to Greece in 1989, establishing EFA VENTURES in Athens.

Under his leadership, EFA VENTURES evolved into a prominent industrial cooperation service provider globally. Today, Hadjiminas oversees EFA GROUP, which includes several international high-tech companies such as THEON SENSORS, SCYTALYS, and ES-SYSTEMS. These companies are integrated through epicos.com, a leading B2B platform for industrial cooperation and offsets, also managed by the Group.

Hadjiminas holds significant positions outside his corporate duties, serving as Vice President of the Hellenic Entrepreneurs Association (EENE) and Head of EENE International. He is also the Founder and Honorary President of the Wharton Alumni Club of Greece.

His commitment to the company is evidenced by his substantial ownership stake, possessing 9.62% of the stock with a current value of $77.2 million. This investment aligns his interests with those of the shareholders, ensuring a shared focus on the value and success of the company.

7. Backlog of orders:

THEON International PLC concluded the fiscal year 2023 with a considerable soft backlog of orders totaling €540 million, accompanied by an additional €520 million in potential options. This significant backlog is primarily slated for invoicing in 2024, highlighting the company's robust pipeline and projected revenue streams

In the first half of 2024, the company reported a reduction in the soft backlog to €427 million. This decrease was largely due to the conversion of some previous backlog orders into recognized revenue. Despite this drawdown, THEON anticipates a resurgence in order intake as the year progresses, particularly towards the end. This expectation is grounded in the company's strategic positioning and market demand, ensuring a strong foundation for meeting their near-term revenue forecasts.

8. Financial Performance:

Revenue Growth: The company has grown revenue at an average CAGR of 50% for the last 5 years, this rapid revenue growth was mostly driven by organic growth.

THEON operates in one of the fastest growing markets in the world with a 11.5% revenue growth CAGR expected for the next few years.

High returns on capital: ROC and ROE are key metrics to evaluate a company because they provide insights on how good the management of the company at capital allocation is. THEON has been able to maintain exceptionally high ROC and ROE for the last years.

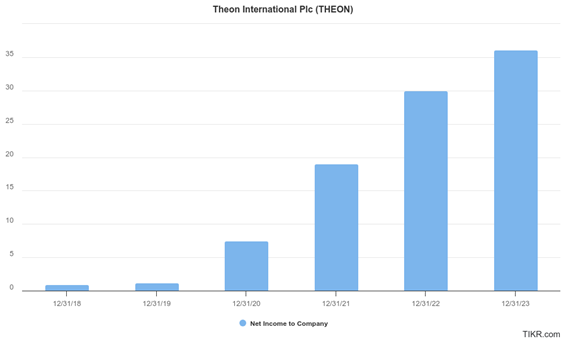

Profitability: The company has been highly profitable for the last 6 years, with margins increasing significantly over the last 6 years. Thanks to the growth in revenue and the improvement in margins the company was able to grow their net income from 0.91M in 2018 to 45.96M in the last twelve months.

9. Thesis:

THEON International PLC presents a compelling investment thesis characterized by both robust long-term earnings growth and promising short-term revenue prospects. Here’s a detailed look at the factors underpinning this positive outlook:

Long-term earnings growth: THEON is strategically positioned to benefit from global increases in military budgets and a strong growth trajectory in the defense market. As nations worldwide expand their defense spending, THEON's cutting-edge products in night vision and thermal imaging systems are poised to see heightened demand. This scenario sets the stage for sustained growth in earnings over the long term.

Short-term growth catalysts: The company's short-term growth is bolstered by a significant backlog of orders, the company’s guidance that was reaffirmed in the last trading update is for revenues to be between 330-350M while maintaining EBIT margins in the mid-20s, if we value the company as of their future FY2024 earnings we see that THEON is currently trading at 8 times EV/EBIT, an attractive valuation for a company with strong growth prospects.

Exceptional return on capital (ROC): THEON consistently demonstrates a great Return on Capital, highlighting its efficiency in using invested funds to generate profits and to achieve profitable growth in the future.

Inorganic growth through acquisitions: Following its recent initial public offering (IPO), THEON is actively pursuing acquisitions. The capital raised from the IPO is earmarked for strategic acquisitions that will allow THEON to expand its technological base and market reach. These acquisitions are intended to complement its existing portfolio, enter new markets, and enhance its competitive edge in the global defense industry, according to the last trading update of THEON the next acquisition will be announced within a few weeks.

EPS growth, combined with a growing dividend and multiple expansion, might lead to substantial returns for the company's shareholders

10. Valuation:

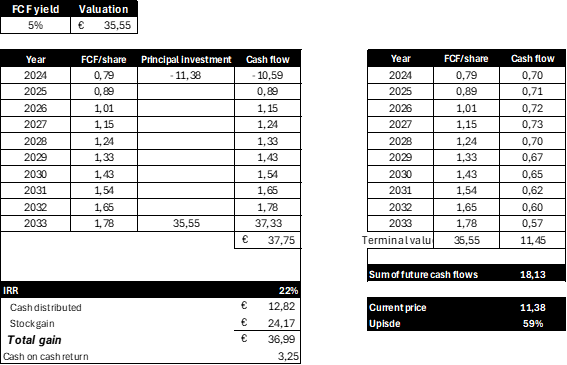

To value THEON International, I have developed a detailed financial forecast extending over the next decade, guided by the following core assumptions:

1. Revenue Growth: Over the next three years, I anticipate a CAGR of 13.5% for THEON, driven by an 11.5% growth from addressable market growth in addition to incremental market share gains and the company's strategic entry into new international markets. After this period, I project a more conservative annual growth rate of 7.5% for the remainder of the forecast period, reflecting slower addressable market growth.

2. Valuation Multiple: For the future trading multiple, I expect the stock to trade at a free cash flow (FCF) yield of 5%. Given the short time the company has been public, I cannot use historical averages to determine this multiple. However, a 5% FCF yield is conservative for a company in the defense sector.

3. Profit Margins and Taxes: I forecast that THEON will sustain its EBIT margin at 26.4% across the forecast horizon. Additionally, I anticipate the tax rate will remain constant at 25%.

4. Capital Expenditures and Dilution: Given THEON’s established profitability and operational cash flow, I do not foresee any share dilution in the foreseeable future. The company’s CAPEX is expected to remain at historical levels (3.5%),

These valuation assumptions are crafted to provide a conservative yet realistic view of THEON’s financial trajectory, ensuring that the estimated company value is grounded in attainable financial performance metrics.

These are the income and cash flow statements forecasted until the year 2033.

To calculate the current value of the stock, I have built an IRR model and a DCF model.

At the current price the stock has a 59% upside and could offer a 22% IRR for the next decade. The current value of future cash flows has been calculated using a WACC of 12%.

11. Risks:

Investing in THEON International entails certain risks that potential investors should consider:

1. Government budget constraints: A significant portion of THEON's revenue comes from contracts with various governments worldwide. Many of these governments are currently facing high levels of debt, which could prompt austerity measures including cuts to defense spending. If such budgetary constraints are implemented, THEON could see a reduction in new contracts or delays in the fulfillment of existing ones, impacting the company's revenue streams.

2. Market competition: While THEON has established a strong position in the night vision and thermal imaging market, the high margins and growth potential in this sector could attract new competitors. Increased competition might lead to price pressures, higher marketing and sales costs, and the need for continuous innovation to maintain market share. This could potentially erode THEON's profitability and market position if not managed effectively.

12. Conclusion:

THEON International presents an interesting investment opportunity as the stock seems quite undervalued, revenue growth in addition to great profitability will be the key drivers for shareholder returns. When the company proves to the market that they can grow sustainably it is very likely that we will see a multiple expansion.

With most companies operating in high growth markets being overvalued, THEON International allows investors to invest in growth without the expensive valuations that investors are having to pay in other markets.

Could you make an update on this company?

If you are interested, I made my own post on Theon: https://mimeticinvesting.substack.com/p/while-this-company-makes-you-look