A Deep Dive into Sibanye ($SBSW): Unlocking a 5x Upside on PGM Prices

High-Cost Assets, High Reward: Why a Price Spike Magnifies Sibanye’s Gains

Investment Report

Key points:

High Leverage to PGM Prices: With around 70% of revenue from PGMs, Sibanye-Stillwater’s legacy high-cost operations offer substantial upside if prices rebound.

Strategic U.S. PGM Assets: U.S. mines and recycling operations are particularly valuable, given geopolitical uncertainties around palladium supply and potential trade issues with Russia.

Sum-of-the-Parts Approach: From gold and PGMs to uranium and other minerals, various segments contribute to Sibanye’s valuation, offering both downside protection and significant upside.

Index:

Introduction

Gold mining and DRDGOLD stake:

PGM mining:

Lithium and battery recycling plants:

Uranium reserves:

Other minerals, Nickel and Zinc

Liquidity and financial position of the group

Other ventures:

Final valuation

As you might know, I hold a very bullish thesis on PGMs. It is one of those “hated” markets that inevitably draws contrarian investors like myself—rare metals with constrained supply, mostly sourced from just two countries, Russia and South Africa. Factors such as substantial short interest in palladium, the potential hydrogen applications for platinum, and increased demand for these minerals in hybrid vehicles (whose production appears to be growing faster than that of BEVs) all point to a significant rise in PGM prices.

In light of this, I am presenting a thesis on Sibanye-Stillwater (SBSW). I believe it offers tremendous leverage to benefit from this outlook, as its combination of high-cost legacy operations and status as one of the world’s largest PGM miners provides an ideal way to gain exposure to PGM price movements.

1. Introduction:

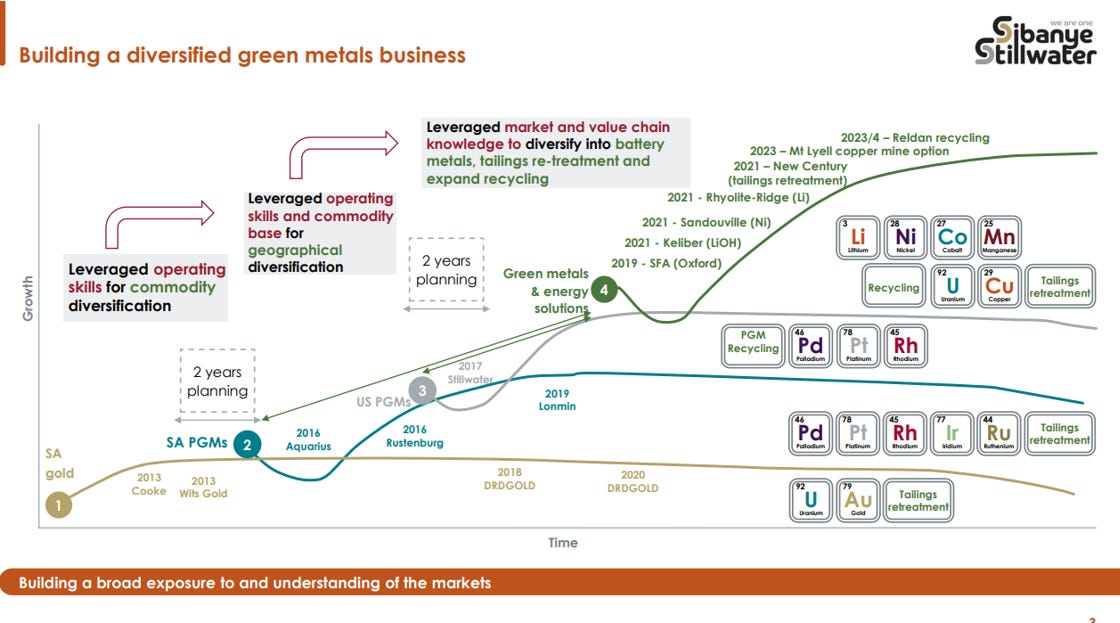

Sibanye is a miner that specializes in green metals, with significant exposure to those needed for the green revolution. However, PGMs still account for around 70% of its revenue, and with prices currently depressed, the stock has suffered a severe decline.

The company’s older assets offer high leverage to PGM and gold prices but also make the stock extremely volatile through commodity cycles. Right now, Sibanye is investing in lithium and battery-related metals, which could provide greater stability in the future and allow the company to benefit from rising demand.

Sibanye Stillwater, often highlighted on Substack, trades on the NYSE and is therefore more accessible to U.S. investors. Over the past decade, the company has outperformed many of its peers. However, it’s also quite complex to value due to its diverse operations:

Gold Mining: Expected to produce over half a million ounces of gold this year.

PGM Mining: Active in both South Africa and the U.S., with a significant portion of PGM production coming from recycling.

Lithium Assets: Owns what is claimed to be the largest lithium mine in Europe, plus a battery recycling plant.

Byproducts and Other Minerals:

Chrome byproduct from PGM mining.

Around 60 million pounds of uranium in tailings; recently entered a joint venture for the Beisa uranium project. Sibanye will receive a cash payment, 40% equity in Neo Energy, and royalties of up to $5/lb of uranium—potentially significant if prices rise.

DRD Gold Stake: Holds 50% of DRD Gold, which has a market cap of nearly $1 billion, valuing Sibanye’s stake at around $490 million.

Streaming Deal: Raised $500 million from Franco-Nevada by pre-selling gold and PGMs from South African operations.

At current PGM prices, Sibanye’s PGM operations are under pressure. U.S. production costs are roughly $1,400 per ounce, while South African costs are somewhat lower, yet still significantly higher than those of competitors like Impala and Anglo American. In response, Sibanye has placed the Stillwater West Mine on care and maintenance and reduced its workforce to lower costs until prices recover.

Overall, the company is highly leveraged to gold and especially PGM prices, and it aims to diversify through lithium and other metals. The thesis for Sibanye is straightforward: it has substantial leverage to PGM prices, while its other assets could offer some stability over the long term.

2. Gold mining and DRDGOLD stake:

The company’s gold operations have an average AISC of around $2,250 per ounce. These high costs stem from older, less efficient mines, but they also create substantial leverage to current gold prices, which are near all-time highs. Despite this, the segment’s value is not fully reflected in the stock price. Conservative estimates suggest that gold alone could justify half of Sibanye’s enterprise value.

With an expected production of about 600,000 ounces of gold at the current price of $2,900 per ounce, these operations could generate close to $400 million in EBITDA. Even using a 4x EBITDA multiple, the gold segment would be worth around $1.6 billion; applying a more conservative 2.5x multiple, primarily due to high costs, still implies around $1 billion in valuation.

DRDGOLD, which has an AISC of approximately $1,600, is currently valued by the public market at around $1 billion. Sibanye’s 50% stake in DRDGOLD is thus worth about $460 million at current prices. Since DRDGOLD trades at about 5x EBITDA, which is arguably lower than the sector average, it is not considered an expensive valuation.

All in all, the gold mining business alone is worth roughly $1 billion in a conservative or bearish scenario, and potentially $1.6 billion in a more bullish scenario. Adding the $460 million stake in DRDGOLD, Sibanye’s gold segment could account for $2.06 billion of its $4.1 billion enterprise value in a bullish case, and somewhat less in a bearish case.

3. PGM mining:

US

Now it is time for a deep dive into PGM mining. The company’s AISC for its U.S. operations is around $1,400 per 2E ounce, with a perceived basket price below $1,000. However, this is affected by taxes and royalties, and the company expects costs to fall to about $1,150 in the future.

In September, the company announced a restructuring that will reduce PGM production by 200,000 ounces, likely normalizing total U.S. production to around 250,000 2E ounces per year. While AISC costs remain high, they have decreased from nearly $2,000 a year ago, thanks to the restructuring. The plan is to focus on lower volumes for the U.S. operations and aim for an average AISC of around $1,000 per 2E ounce.

These U.S. mines are strategically important because much of the world’s palladium supply comes from Russia and South Africa. If a trade war with BRICS nations were to affect PGM imports, Sibanye’s U.S. assets could become extremely valuable domestically, potentially causing national prices for PGMs to soar. It is also worth noting that about 75% of U.S. production is palladium, which heightens exposure to potential tariffs on Russian palladium.

These positive developments were reinforced on October 24, 2024, when the U.S. Department of the Treasury published final regulations for Section 45X of the Inflation Reduction Act (IRA). Initially passed in August 2022, the IRA aimed to promote domestic clean energy component production, with Section 45X proposing a 10% Advanced Manufacturing Production credit for critical minerals like palladium and platinum. However, guidance issued in December 2023 excluded extraction and processing, providing limited support for U.S. PGM operations. Fortunately, the final S45X rules now include extraction and processing in addition to refining costs, which should provide significant financial support for U.S. PGM operations. While further consultation with tax advisors is needed to confirm the exact impact, initial estimates indicate benefits of about $140 million for 2023 and $100 million for 2024. There is a possibility that these tax benefits—totaling around a quarter of a billion dollars—will continue into the future.