+72.53% Total Return: Calls With New Princes’ CFO and PharmX’s CEO, Monthly Portfolio Update

Management Calls, Earnings Watchlist, and Precious Metals Risk

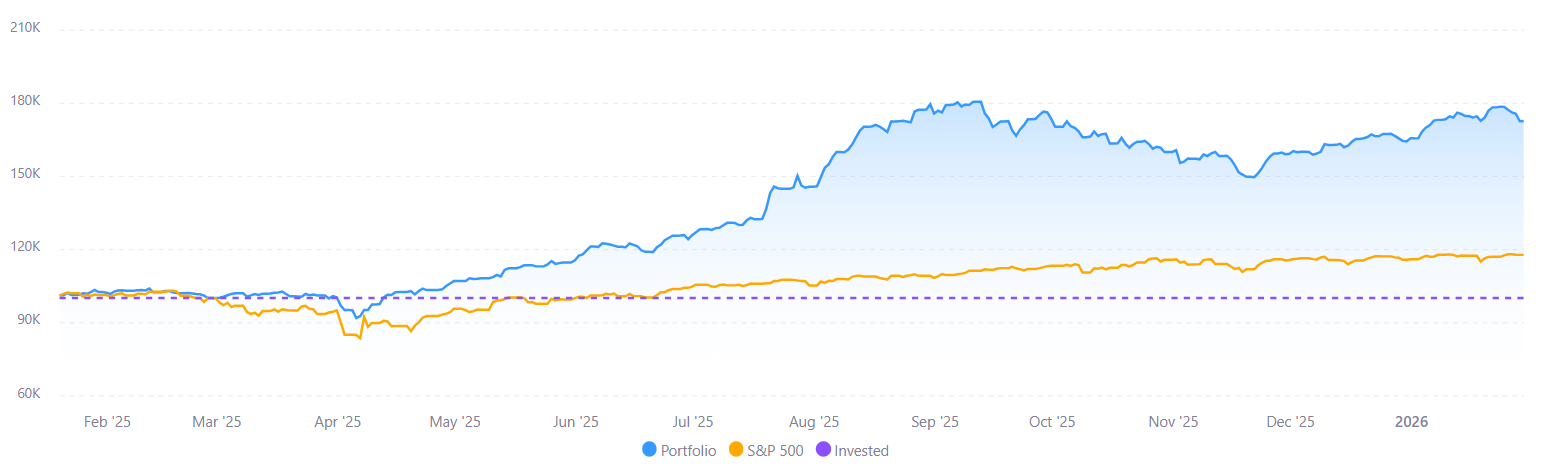

The Buried Bargains portfolio is up 72.53% since its inception on 20 January 2025. Returns for 2025 were 64.3%, and YTD returns so far are 4.96%. This means we are beating the S&P by 56.12%, while running at lower absolute risk than the market. We use no leverage and hold only cheap stocks with low expectations baked in—effectively reducing the most important risk: permanent loss of capital.

Undervalued & Undercovered is an educational research service for professionals who want to save time while still receiving deep dives on high-potential small-cap companies. For premium subscribers, we also provide this model portfolio, helping them size and select the best theses we publish on the platform.

Today it’s time to update you on two management calls we had this week, one with the CEO of PharmX and another with the CFO of New Princes. Very interesting insights on both ends, which we will discuss today.

Additionally, I think it’s time to add some commentary on PGMs and the overall precious metals environment. With some additional notes at the end about some of the companies we believe have a strong profile for their upcoming earnings.

Buried Bargains portfolio vs S&P

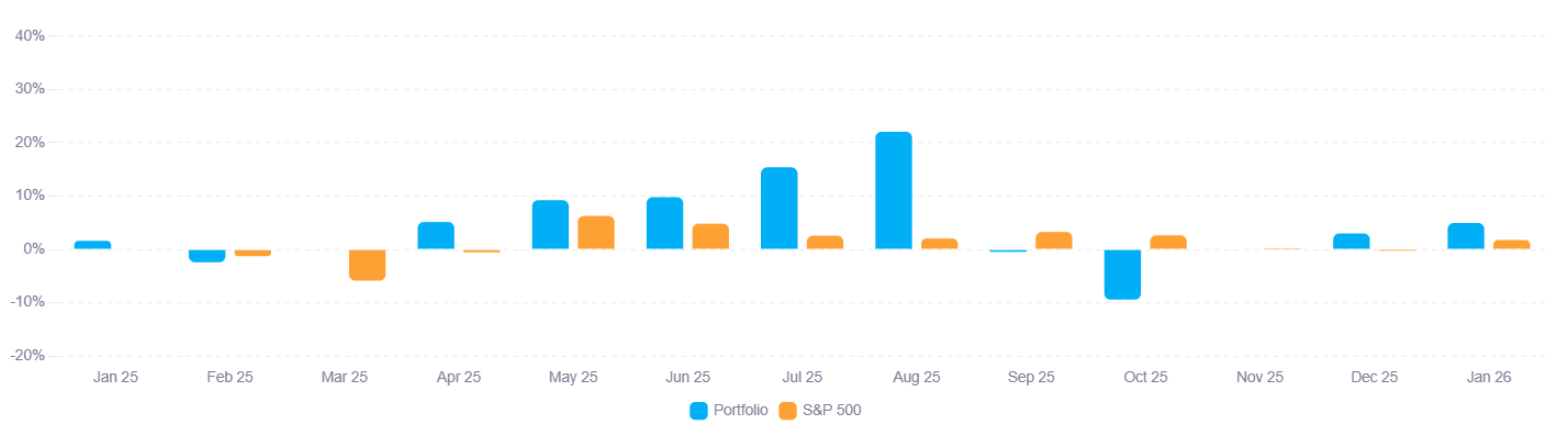

Monthly returns.

Market view:

2026 has started with a bull run for the “old economy”, oil services, miners, Latin America, and the hot topic now being precious metals.

At the moment I am writing this, I just saw gold and silver lose the equivalent of twice the GDP of Spain in a few hours (at the time of posting it’s like 4 times the GDP of Spain). We are at dangerous levels for precious metals; we are seeing crypto-like liquidations in what is supposed to be a safe-haven asset. I’m not sure what that means for the overall economy, but it clearly does not show trust in the system.

I am a big contrarian by nature, and the overly strong consensus on precious metals being a long is quite concerning to me. It’s clearly an area that has been underinvested for a long time. But current price chasing is pure speculation. Referring to the chat I had with the CEO of First Tin, what we are seeing currently are fly-ups: supply is not responsive and demand in industrial purposes cares little about prices, and speculators rush to buy, increasing the demand for a short amount of time; this leads to the current fly-up behaviour. But this does not mean that these prices will be maintained for long or that the long-term average price is suddenly 120 for silver. It’s always the same game: as long as prices are above incentive prices for new projects to emerge, we will have new supply. People right now are betting (and with good reasoning) that current fly-up behaviour will just continue because new supply will just take too long. Every metal is different and some can actually sit on much higher long-term averages; tin, in my view, will do that. But chasing the current rally is dangerous; miners are cheap because investors realize that. Fly-ups are a bonus, not what you would expect as the 10-year average price you will sell your production for.

Be rational and avoid trend chasing, not much more to say, and if you want to believe that this time will be different and that physics and incentives do not work, best of luck for you, you might win, great if speculating is your game, but I invest and I do not want to take the risk of a -50% if something happens with the economy and demand for these metals tanks, while chasing another quick and volatile 2x.

That said, the mining sector is cheap, commodities are underinvested, Latin America and small caps are cheap, there is a ton of stuff that is interesting and it’s still interesting despite a good month of January. So continue looking for opportunities there, just avoid things that are already crowded and learn to avoid FOMO.

I have had a meaningful position in PGMs since January 2025, so I am sitting on substantial gains from there. I am now taking profits on those positions, miners, and direct commodity exposure. It’s been a great rally and maybe we get another 50% up, who knows. I’ve still got some exposure which will allow me to get some extra profits from this continued fly-up behaviour which we will likely see over the next 12 months, however having PGMs as my main position was just not a smart move right now. Sylvania Platinum is still probably the cheapest name out there, it has been over a 3x for me, it’s still at a really low single-digit valuation at current prices, so I would recommend the trend-chasing investors to take a look at that one, at least you will have a better risk-reward profile.

Independent trends:

In today’s market it seems like everything is based on the same trends: currency debasement, tech, AI, data centers, Ponzi-like schemes, going back to ultra-low interest rates. What can we do in the current market to protect ourselves? The obvious answer is to buy value, boring value plays in defensive sectors. But not going to lie, every time it’s more difficult to find safety and good upside potential in today’s market. An attractive setup that prevails in current times and can deliver attractive risk-adjusted returns while relying less on the overall market mood are what I call independent trend players. Those players tend to share two characteristics: they are small and also they will ride an upcoming trend which is so niche that people do not follow it, and the company is also small which means that it’s priced very inaccurately. Let me give you two examples:

First of all, Seeing Machines, this year every car in Europe will need to have a camera-based DMS system, that’s by law, starting this July. If that comes into effect their market will go from 1-2 million cars a year to 16 million cars, an 8x in volumes; do you think it really matters if we go into a recession and only 14 million cars are sold? It’s still a 7x in volumes and the market does not price correctly that possibility just because it is so niche. If you are interested and would like to read more, I leave here the article I made after talking with the CEO and CFO:

Another favourite of mine is Australian childcare, with new increased subsidies that will increase demand and will be great drivers for already founder-led roll-up operators trading at bargain valuations.

I also think that PharmX is another one of those setups, in my opinion: high quality business, earns fees based on Australian pharmacy volumes, and its growth strategy is solely execution dependent.

These types of setups are those that excite me in the current market, in combination with some defensive sector exposure, really cheap names, and a good cash position to increase your position size opportunistically; that is my sweet spot where I feel comfortable in the current market.

Portfolio review + management calls:

Now its time to review the portfolio, but more importantly to update on my last two management calls, one with Tom Culver the CEO of PharmX and another one with Fabio Fazzari the CFO of New Princes group.

So far our performance is good, but in comfort lays a lot of dangers, its always important to reassess your thesis and conviction in all of your positions.

The exact current positioning: